Indian Accounting Standard (Ind AS) 11

Construction Contracts

(This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type indicate the main principles.)

Objective

The objective of this Standard is to prescribe the accounting treatment of revenue and costs associated with construction contracts. Because of the nature of the activity undertaken in construction contracts, the date at which the contract activity is entered into and the date when the activity is completed usually fall into different accounting periods. Therefore, the primary issue in accounting for construction contracts is the allocation of contract revenue and contract costs to the accounting periods in which construction work is performed. This Standard uses the recognition criteria established in the Framework for the Preparation and Presentation of Financial Statements issued by the Institute of Chartered Accountants of India to determine when contract revenue and contract costs should be recognised as revenue and expenses in the statement of profit and loss. It also provides practical guidance on the application of these criteria.

Scope

1. This Standard shall be applied in accounting for construction contracts in the financial statements of contractors.

1A The impairment of any contractual right to receive cash or another financial asset arising from this Standard

shall be dealt in accordance with Ind AS 109, Financial Instruments.

2. *

Definitions

3. The following terms are used in this Standard with the meanings specified:

A construction contract is a contract specifically negotiated for the construction of an asset or a combination of assets that are closely interrelated or interdependent in terms of their design, technology and function or their ultimate purpose or use.

A fixed price contract is a construction contract in which the contractor agrees to a fixed contract price, or a fixed rate per unit of output, which in some cases is subject to cost escalation clauses.

A cost plus contract is a construction contract in which the contractor is reimbursed for allowable or otherwise defined costs, plus a percentage of these costs or a fixed fee.

4. A construction contract may be negotiated for the construction of a single asset such as a bridge, building, dam, pipeline, road, ship or tunnel. A construction contract may also deal with the construction of a number of assets which are closely interrelated or interdependent in terms of their design, technology and function or their ultimate purpose or use; examples of such contracts include those for the construction of refineries and other complex pieces of plant or equipment.

5. For the purposes of this Standard, construction contracts include:

(a) contracts for the rendering of services which are directly related to the construction of the asset, for example, those for the services of project managers and architects; and

(b) contracts for the destruction or restoration of assets, and the restoration of the environment following the demolition of assets.

6. Construction contracts are formulated in a number of ways which, for the purposes of this Standard, are classified as fixed price contracts and cost plus contracts. Some construction contracts may contain characteristics of both a fixed price contract and a cost plus contract, for example in the case of a cost plus contract with an agreed maximum price. In such circumstances, a contractor needs to consider all the conditions in paragraphs 23 and 24 in order to determine when to recognise contract revenue and expenses.

Combining and segmenting construction contracts

7. The requirements of this Standard are usually applied separately to each construction contract. However, in certain circumstances, it is necessary to apply the Standard to the separately identifiable components of a single contract or to a group of contracts together in order to reflect the substance of a contract or a group of contracts.

8. When a contract covers a number of assets, the construction of each asset shall be treated as a separate construction contract when:

(a) separate proposals have been submitted for each asset;

(b) each asset has been subject to separate negotiation and the contractor and customer have been able to accept or reject that part of the contract relating to each asset; and

(c) the costs and revenues of each asset can be identified.

9. A group of contracts, whether with a single customer or with several customers, shall be treated as a single construction contract when:

(a) the group of contracts is negotiated as a single package;

(b) the contracts are so closely interrelated that they are, in effect, part of a single project with an overall profit margin; and

(c) the contracts are performed concurrently or in a continuous sequence.

10. A contract may provide for the construction of an additional asset at the option of the customer or may be amended to include the construction of an additional asset. The construction of the additional asset shall be treated as a separate construction contract when:

(a) the asset differs significantly in design, technology or function from the asset or assets covered by the original contract; or

(b) the price of the asset is negotiated without regard to the original contract price.

Contract revenue

11. Contract revenue shall comprise:

(a) the initial amount of revenue agreed in the contract; and

(b) variations in contract work, claims and incentive payments:

(i) to the extent that it is probable that they will result in revenue; and

(ii) they are capable of being reliably measured.

12. Contract revenue is measured at the fair value of the consideration received or receivable. The measurement of contract revenue is affected by a variety of uncertainties that depend on the outcome of future events. The estimates often need to be revised as events occur and uncertainties are resolved. Therefore, the amount of contract revenue may increase or decrease from one period to the next. For example:

(a) a contractor and a customer may agree variations or claims that increase or decrease contract revenue in a period subsequent to that in which the contract was initially agreed;

(b) the amount of revenue agreed in a fixed price contract may increase as a result of cost escalation clauses;

(c) the amount of contract revenue may decrease as a result of penalties arising from delays caused by the contractor in the completion of the contract; or

(d) when a fixed price contract involves a fixed price per unit of output, contract revenue increases as the number of units is increased.

13. A variation is an instruction by the customer for a change in the scope of the work to be performed under the contract. A variation may lead to an increase or a decrease in contract revenue. Examples of variations are changes in the specifications or design of the asset and changes in the duration of the contract. A variation is included in contract revenue when:

(a) it is probable that the customer will approve the variation and the amount of revenue arising from the variation; and

(b) the amount of revenue can be reliably measured.

14. A claim is an amount that the contractor seeks to collect from the customer or another party as reimbursement for costs not included in the contract price. A claim may arise from, for example, customer caused delays, errors in specifications or design, and disputed variations in contract work. The measurement of the amounts of revenue arising from claims is subject to a high level of uncertainty and often depends on the outcome of negotiations. Therefore, claims are included in contract revenue only when:

(a) negotiations have reached an advanced stage such that it is probable that the customer will accept the claim; and

(b) the amount that it is probable will be accepted by the customer can be measured reliably.

15. Incentive payments are additional amounts paid to the contractor if specified performance standards are met or exceeded. For example, a contract may allow for an incentive payment to the contractor for early completion of the contract. Incentive payments are included in contract revenue when:

(a) the contract is sufficiently advanced that it is probable that the specified performance standards will be met or exceeded; and

(b) the amount of the incentive payment can be measured reliably.

Contract costs

16. Contract costs shall comprise:

(a) costs that relate directly to the specific contract;

(b) costs that are attributable to contract activity in general and can be allocated to the contract; and

(c) such other costs as are specifically chargeable to the customer under the terms of the contract.

17. Costs that relate directly to a specific contract include:

(a) site labour costs, including site supervision;

(b) costs of materials used in construction;

(c) depreciation of plant and equipment used on the contract;

(d) costs of moving plant, equipment and materials to and from the contract site;

(e) costs of hiring plant and equipment;

(f) costs of design and technical assistance that is directly related to the contract;

(g) the estimated costs of rectification and guarantee work, including expected warranty costs; and

(h) claims from third parties.

These costs may be reduced by any incidental income that is not included in contract revenue, for example income from the sale of surplus materials and the disposal of plant and equipment at the end of the contract.

18. Costs that may be attributable to contract activity in general and can be allocated to specific contracts include:

(a) insurance;

(b) costs of design and technical assistance that are not directly related to a specific contract; and

(c) construction overheads.

Such costs are allocated using methods that are systematic and rational and are applied consistently to all costs having similar characteristics. The allocation is based on the normal level of construction activity. Construction overheads include costs such as the preparation and processing of construction personnel payroll. Costs that may be attributable to contract activity in general and can be allocated to specific contracts also include borrowing costs.

19. Costs that are specifically chargeable to the customer under the terms of the contract may include some general administration costs and development costs for which reimbursement is specified in the terms of the contract.

20. Costs that cannot be attributed to contract activity or cannot be allocated to a contract are excluded from the costs of a construction contract. Such costs include:

(a) general administration costs for which reimbursement is not specified in the contract;

(b) selling costs;

(c) research and development costs for which reimbursement is not specified in the contract; and

(d) depreciation of idle plant and equipment that is not used on a particular contract.

21. Contract costs include the costs attributable to a contract for the period from the date of securing the contract to the final completion of the contract. However, costs that relate directly to a contract and are incurred in securing the contract are also included as part of the contract costs if they can be separately identified and measured reliably and it is probable that the contract will be obtained. When costs incurred in securing a contract are recognised as an expense in the period in which they are incurred, they are not included in contract costs when the contract is obtained in a subsequent period.

Recognition of contract revenue and expenses

22. When the outcome of a construction contract can be estimated reliably, contract revenue and contract costs associated with the construction contract shall be recognised as revenue and expenses respectively by reference to the stage of completion of the contract activity at the end of the reporting period. An expected loss on the construction contract shall be recognised as an expense immediately in accordance with paragraph 36.

23. In the case of a fixed price contract, the outcome of a construction contract can be estimated reliably when all the following conditions are satisfied:

(a) total contract revenue can be measured reliably;

(b) it is probable that the economic benefits associated with the contract will flow to the entity;

(c) both the contract costs to complete the contract and the stage of contract completion at the end of the reporting period can be measured reliably; and

(d) the contract costs attributable to the contract can be clearly identified and measured reliably so that actual contract costs incurred can be compared with prior estimates.

24. In the case of a cost plus contract, the outcome of a construction contract can be estimated reliably when all the following conditions are satisfied:

(a) it is probable that the economic benefits associated with the contract will flow to the entity; and

(b) the contract costs attributable to the contract, whether or not specifically reimbursable, can be clearly identified and measured reliably.

25. The recognition of revenue and expenses by reference to the stage of completion of a contract is often referred to as the percentage of completion method. Under this method, contract revenue is matched with the contract costs incurred in reaching the stage of completion, resulting in the reporting of revenue, expenses and profit which can be attributed to the proportion of work completed. This method provides useful information on the extent of contract activity and performance during a period.

26. Under the percentage of completion method, contract revenue is recognised as revenue in profit or loss in the accounting periods in which the work is performed. Contract costs are usually recognised as an expense in profit or loss in the accounting periods in which the work to which they relate is performed. However, any expected excess of total contract costs over total contract revenue for the contract is recognised as an expense immediately in accordance with paragraph 36.

27. A contractor may have incurred contract costs that relate to future activity on the contract. Such contract costs are recognised as an asset provided it is probable that they will be recovered. Such costs represent an amount due from the customer and are often classified as contract work in progress.

28. The outcome of a construction contract can only be estimated reliably when it is probable that the economic benefits associated with the contract will flow to the entity. However, when an uncertainty arises about the collectibility of an amount already included in contract revenue, and already recognised in profit or loss, the uncollectible amount or the amount in respect of which recovery has ceased to be probable is recognised as an expense rather than as an adjustment of the amount of contract revenue.

29. An entity is generally able to make reliable estimates after it has agreed to a contract which establishes:

(a) each party’s enforceable rights regarding the asset to be constructed;

(b) the consideration to be exchanged; and

(c) the manner and terms of settlement.

It is also usually necessary for the entity to have an effective internal financial budgeting and reporting system. The entity reviews and, when necessary, revises the estimates of contract revenue and contract costs as the contract progresses. The need for such revisions does not necessarily indicate that the outcome of the contract cannot be estimated reliably.

30. The stage of completion of a contract may be determined in a variety of ways. The entity uses the method that measures reliably the work performed. Depending on the nature of the contract, the methods may include:

(a) the proportion that contract costs incurred for work performed to date bear to the estimated total contract costs;

(b) surveys of work performed; or

(c) completion of a physical proportion of the contract work.

Progress payments and advances received from customers often do not reflect the work performed.

31. When the stage of completion is determined by reference to the contract costs incurred to date, only those contract costs that reflect work performed are included in costs incurred to date. Examples of contract costs which are excluded are:

(a) contract costs that relate to future activity on the contract, such as costs of materials that have been delivered to a contract site or set aside for use in a contract but not yet installed, used or applied during contract performance, unless the materials have been made specially for the contract; and

(b) payments made to subcontractors in advance of work performed under the subcontract.

32. When the outcome of a construction contract cannot be estimated reliably:

(a) revenue shall be recognised only to the extent of contract costs incurred that it is probable will be recoverable; and

(b) contract costs shall be recognised as an expense in the period in which they are incurred.

An expected loss on the construction contract shall be recognised as an expense immediately in accordance with paragraph 36.

33. During the early stages of a contract it is often the case that the outcome of the contract cannot be estimated reliably. Nevertheless, it may be probable that the entity will recover the contract costs incurred. Therefore, contract revenue is recognised only to the extent of costs incurred that are expected to be recoverable. As the outcome of the contract cannot be estimated reliably, no profit is recognised. However, even though the outcome of the contract cannot be estimated reliably, it may be probable that total contract costs will exceed total contract revenues. In such cases, any expected excess of total contract costs over total contract revenue for the contract is recognised as an expense immediately in accordance with paragraph 36.

34. Contract costs that are not probable of being recovered are recognised as an expense immediately. Examples of circumstances in which the recoverability of contract costs incurred may not be probable and in which contract costs may need to be recognised as an expense immediately include contracts:

(a) that are not fully enforceable, ie their validity is seriously in question;

(b) the completion of which is subject to the outcome of pending litigation or legislation;

(c) relating to properties that are likely to be condemned or expropriated;

(d) where the customer is unable to meet its obligations; or

(e) where the contractor is unable to complete the contract or otherwise meet its obligations under the contract.

35. When the uncertainties that prevented the outcome of the contract being estimated reliably no longer exist, revenue and expenses associated with the construction contract shall be recognised in accordance with paragraph 22 rather than in accordance with paragraph 32.

Recognition of expected losses

36. When it is probable that total contract costs will exceed total contract revenue, the expected loss shall be recognised as an expense immediately.

37. The amount of such a loss is determined irrespective of:

(a) whether work has commenced on the contract;

(b) the stage of completion of contract activity; or

(c) the amount of profits expected to arise on other contracts which are not treated as a single construction contract in accordance with paragraph 9.

Changes in estimates

38. The percentage of completion method is applied on a cumulative basis in each accounting period to the current estimates of contract revenue and contract costs. Therefore, the effect of a change in the estimate of contract revenue or contract costs, or the effect of a change in the estimate of the outcome of a contract, is accounted for as a change in accounting estimate (see Ind AS 8, Accounting Policies, Changes in Accounting Estimates and Errors). The changed estimates are used in the determination of the amount of revenue and expenses recognised in profit or loss in the period in which the change is made and in subsequent periods.

Disclosure

39. An entity shall disclose:

(a) the amount of contract revenue recognised as revenue in the period;

(b) the methods used to determine the contract revenue recognised in the period; and

(c) the methods used to determine the stage of completion of contracts in progress.

40. An entity shall disclose each of the following for contracts in progress at the end of the reporting period:

(a) the aggregate amount of costs incurred and recognised profits (less recognised losses) to date;

(b) the amount of advances received; and

(c) the amount of retentions.

41. Retentions are amounts of progress billings that are not paid until the satisfaction of conditions specified in the contract for the payment of such amounts or until defects have been rectified. Progress billings are amounts billed for work performed on a contract whether or not they have been paid by the customer. Advances are amounts received by the contractor before the related work is performed.

42. An entity shall present:

(a) the gross amount due from customers for contract work as an asset; and

(b) the gross amount due to customers for contract work as a liability.

43. The gross amount due from customers for contract work is the net amount of:

(a) costs incurred plus recognised profits; less

(b) the sum of recognised losses and progress billings

for all contracts in progress for which costs incurred plus recognised profits (less recognised losses) exceeds progress billings.

44. The gross amount due to customers for contract work is the net amount of:

(a) costs incurred plus recognised profits; less

(b) the sum of recognised losses and progress billings

for all contracts in progress for which progress billings exceed costs incurred plus recognised profits (less recognised losses).

45. An entity discloses any contingent liabilities and contingent assets in accordance with Ind AS 37, Provisions, Contingent Liabilities and Contingent Assets. Contingent liabilities and contingent assets may arise from such items as warranty costs, claims, penalties or possible losses.

Appendix A

Service Concession Arrangements

This Appendix is an integral part of Indian Accounting Standard (Ind AS)

Background

1 Infrastructure for public services—such as roads, bridges, tunnels, prisons, hospitals, airports, water distribution facilities, energy supply and telecommunication networks—has traditionally been constructed, operated and maintained by the public sector and financed through public budget appropriation.

2 In recent times, governments have introduced contractual service arrangements to attract private sector participation in the development, financing, operation and maintenance of such infrastructure. The infrastructure may already exist, or may be constructed during the period of the service arrangement. An arrangement within the scope of this Appendix typically involves a private sector entity (an operator) constructing the infrastructure used to provide the public service or upgrading it (for example, by increasing its capacity) and operating and maintaining that infrastructure for a specified period of time. The operator is paid for its services over the period of the arrangement. The arrangement is governed by a contract that sets out performance standards, mechanisms for adjusting prices, and arrangements for arbitrating disputes. Such an arrangement is often described as a ‘build-operate-transfer’, a ‘rehabilitate-operate-transfer’ or a ‘public-to-private’ service concession arrangement.

3 A feature of these service arrangements is the public service nature of the obligation undertaken by the operator. Public policy is for the services related to the infrastructure to be provided to the public, irrespective of the identity of the party that operates the services. The service arrangement contractually obliges the operator to provide the services to the public on behalf of the public sector entity. Other common features are:

(a) the party that grants the service arrangement (the grantor) is a public sector entity, including a governmental body, or a private sector entity to which the responsibility for the service has been devolved.

(b) the operator is responsible for at least some of the management of the infrastructure and related services and does not merely act as an agent on behalf of the grantor.

(c) the contract sets the initial prices to be levied by the operator and regulates price revisions over the period of the service arrangement.

(d) the operator is obliged to hand over the infrastructure to the grantor in a specified condition at the end of the period of the arrangement, for little or no incremental consideration, irrespective of which party initially financed it.

Scope

4 This Appendix gives guidance on the accounting by operators for public-to-private service concession arrangements

5 This Appendix applies to public-to-private service concession arrangements if:

(a) the grantor controls or regulates what services the operator must provide with the infrastructure, to whom it must provide them, and at what price; and

(b) the grantor controls—through ownership, beneficial entitlement or otherwise—any significant residual interest in the infrastructure at the end of the term of the arrangement.

6. Infrastructure used in a public-to-private service concession arrangement for its entire useful life (whole of life assets) is within the scope of this Appendix if the conditions in paragraph 5(a) of this Appendix are met. Paragraphs AG1–AG8 of the Application Guidance of this Appendix provide guidance on determining whether, and to what extent, public-to-private service concession arrangements are within the scope of this Appendix.

7 This Appendix applies to both:

(a) infrastructure that the operator constructs or acquires from a third party for the purpose of the service arrangement; and

(b) existing infrastructure to which the grantor gives the operator access for the purpose of the service arrangement.

8 This Appendix does not specify the accounting for infrastructure that was held and recognised as property, plant and equipment by the operator before entering the service arrangement. The derecognition requirements of Indian Accounting Standards (as set out in Ind AS 16 ) apply to such infrastructure.

9 This Appendix does not specify the accounting by grantors.

Issues

10 This Appendix sets out general principles on recognising and measuring the obligations and related rights in service concession arrangements. Requirements for disclosing information about service concession arrangements are in Appendix B to this Indian Accounting Standard. The issues addressed in this Appendix are:

(a) treatment of the operator’s rights over the infrastructure;

(b) recognition and measurement of arrangement consideration;

(c) construction or upgrade services;

(d) operation services;

(e) borrowing costs;

(f) subsequent accounting treatment of a financial asset and an intangible asset; and

(g) items provided to the operator by the grantor.

Accounting Principles

Treatment of the operator’s rights over the infrastructure

11 Infrastructure within the scope of this Appendix shall not be recognised as property, plant and equipment of the operator because the contractual service arrangement does not convey the right to control the use of the public service infrastructure to the operator. The operator has access to operate the infrastructure to provide the public service on behalf of the grantor in accordance with the terms specified in the contract.

Recognition and measurement of arrangement consideration

12 Under the terms of contractual arrangements within the scope of this Appendix, the operator acts as a service provider. The operator constructs or upgrades infrastructure (construction or upgrade services) used to provide a public service and operates and maintains that infrastructure (operation services) for a specified period of time.

13 The operator shall recognise and measure revenue in accordance with Ind AS 11 and Ind AS 18 for the services it performs. If the operator performs more than one service (ie construction or upgrade services and operation services) under a single contract or arrangement, consideration received or receivable shall be allocated by reference to the relative fair values of the services delivered, when the amounts are separately identifiable. The nature of the consideration determines its subsequent accounting treatment. The subsequent accounting for consideration received as a financial asset and as an intangible asset is detailed in paragraphs 23–26 below.

Construction or upgrade services

14 The operator shall account for revenue and costs relating to construction or upgrade services in accordance with this standard.

Consideration given by the grantor to the operator

15 If the operator provides construction or upgrade services the consideration received or receivable by the operator shall be recognized at its fair value. The consideration may be rights to:

(a) a financial asset, or

(b) an intangible asset.

16 The operator shall recognise a financial asset to the extent that it has an unconditional contractual right to receive cash or another financial asset from or at the direction of the grantor for the construction services; the grantor has little, if any, discretion to avoid payment, usually because the agreement is enforceable by law. The operator has an unconditional right to receive cash if the grantor contractually guarantees to pay the operator (a) specified or determinable amounts or (b) the shortfall, if any, between amounts received from users of the public service and specified or determinable amounts, even if payment is contingent on the operator ensuring that the infrastructure meets specified quality or efficiency requirements.

17 The operator shall recognise an intangible asset to the extent that it receives a right (a licence) to charge users of the public service. A right to charge users of the public service is not an unconditional right to receive cash because the amounts are contingent on the extent that the public uses the service.

18 If the operator is paid for the construction services partly by a financial asset and partly by an intangible asset it is necessary to account separately for each component of the operator’s consideration. The consideration received or receivable for both components shall be recognised initially at the fair value of the consideration received or

receivable.

19 The nature of the consideration given by the grantor to the operator shall be determined by reference to the contract terms and, when it exists, relevant contract law.

Operation services

20 The operator shall account for revenue and costs relating to operation services in accordance with Ind AS 18.

Contractual obligations to restore the infrastructure to a specified level of serviceability

21 The operator may have contractual obligations it must fulfil as a condition of its licence

(a) to maintain the infrastructure to a specified level of serviceability or (b) to restore the infrastructure to a specified condition before it is handed over to the grantor at the end of the service arrangement. These contractual obligations to maintain or restore infrastructure, except for any upgrade element (see paragraph 14 of this Appendix), shall be recognised and measured in accordance with Ind AS 37, ie at the best estimate of the expenditure that would be required to settle the present obligation at the end of the reporting period.

Borrowing costs incurred by the operator

22 In accordance with Ind AS 23, borrowing costs attributable to the arrangement shall be recognised as an expense in the period in which they are incurred unless the operator has a contractual right to receive an intangible asset (a right to charge users of the public service). In this case borrowing costs attributable to the arrangement shall be capitalised during the construction phase of the arrangement in accordance with that Standard.

Financial asset

23 Ind AS 32, Ind AS 107 and Ind AS 109 apply to the financial asset recognised under paragraphs 16 and 18 of this Appendix.

24 The amount due from or at the direction of the grantor is accounted for in accordance with Ind AS 109 at:

(a) amortised cost;

(b) fair value through other comprehensive income; or

(c) fair value through profit or loss.

25 If the amount due from the grantor is measured at amortised cost or fair value through other comprehensive income, Ind AS 109 requires interest calculated using the effective interest method to be recognised in profit or loss.

Intangible asset

26 Ind AS 38 applies to the intangible asset recognised in accordance with paragraphs 17 and 18 of this Appendix. Paragraphs 45–47 of Ind AS 38 provide guidance on measuring intangible assets acquired in exchange for a non-monetary asset or assets or a combination of monetary and non-monetary assets.

Items provided to the operator by the grantor

27 In accordance with paragraph 11, infrastructure items to which the operator is given access by the grantor for the purposes of the service arrangement are not recognised as property, plant and equipment of the operator. The grantor may also provide other items to the operator that the operator can keep or deal with as it wishes. If such assets form part of the consideration payable by the grantor for the services, they are not government grants as defined in Ind AS 20. They are recognised as assets of the operator, measured at fair value on initial recognition. The operator shall recognise a liability in respect of unfulfilled obligations it has assumed in exchange for the assets.

Application Guidance on Appendix A

This Application Guidance is an integral part of Appendix A

Scope (paragraph 5 of Appendix A)

AG1 Paragraph 5 of Appendix A specifies that infrastructure is within the scope of the Appendix when the following conditions apply:

(a) the grantor controls or regulates what services the operator must provide with the infrastructure, to whom it must provide them, and at what price; and

(b) the grantor controls—through ownership, beneficial entitlement or otherwise—any significant residual interest in the infrastructure at the end of the term of the arrangement.

AG2 The control or regulation referred to in condition (a) could be by contract or otherwise (such as through a regulator), and includes circumstances in which the grantor buys all of the output as well as those in which some or all of the output is bought by other users. In applying this condition, the grantor and any related parties shall be considered together. If the grantor is a public sector entity, the public sector as a whole, together with any regulators acting in the public interest, shall be regarded as related to the grantor for the purposes of this Appendix A.

AG3 For the purpose of condition (a), the grantor does not need to have complete control of the price: it is sufficient for the price to be regulated by the grantor, contract or regulator, for example by a capping mechanism. However, the condition shall be applied to the substance of the agreement. Non-substantive features, such as a cap that will apply only in remote circumstances, shall be ignored. Conversely, if for example, a contract purports to give the operator freedom to set prices, but any excess profit is returned to the grantor, the operator’s return is capped and the price element of the control test is met.

AG4 For the purpose of condition (b), the grantor’s control over any significant residual interest should both restrict the operator’s practical ability to sell or pledge the infrastructure and give the grantor a continuing right of use throughout the period of the arrangement. The residual interest in the infrastructure is the estimated current value of the infrastructure as if it were already of the age and in the condition expected at the end of the period of the arrangement.

AG5 Control should be distinguished from management. If the grantor retains both the degree of control described in paragraph 5(a) of Appendix A and any significant residual interest in the infrastructure, the operator is only managing the infrastructure on the grantor’s behalf—even though, in many cases, it may have wide managerial discretion.

AG6 Conditions (a) and (b) together identify when the infrastructure, including any replacements required (see paragraph 21 of Appendix A), is controlled by the grantor for the whole of its economic life. For example, if the operator has to replace part of an item of infrastructure during the period of the arrangement (eg the top layer of a road or the roof of a building), the item of infrastructure shall be considered as a whole. Thus condition (b) is met for the whole of the infrastructure, including the part that is replaced, if the grantor controls any significant residual interest in the final replacement of that part.

AG7 Sometimes the use of infrastructure is partly regulated in the manner described in paragraph 5(a) of Appendix A and partly unregulated. However, these arrangements take a variety of forms:

(a) any infrastructure that is physically separable and capable of being operated independently and meets the definition of a cash-generating unit as defined in Ind AS 36 shall be analysed separately if it is used wholly for unregulated purposes. For example, this might apply to a private wing of a hospital, where the remainder of the hospital is used by the grantor to treat public patients.

(b) when purely ancillary activities (such as a hospital shop) are unregulated, the control tests shall be applied as if those services did not exist, because in cases in which the grantor controls the services in the manner described in paragraph 5 of Appendix A, the existence of ancillary activities does not detract from the grantor’s control of the infrastructure.

AG8 The operator may have a right to use the separable infrastructure described in paragraph AG7 (a), or the facilities used to provide ancillary unregulated services described in paragraph AG7 (b). In either case, there may in substance be a lease from the grantor to the operator; if so, it shall be accounted for in accordance with Ind AS 17.

Information note 1

Accounting framework for public-to-private service arrangements

This note accompanies, but is not part of, Appendix A

The diagram below summarises the accounting for service arrangements established by Appendix A

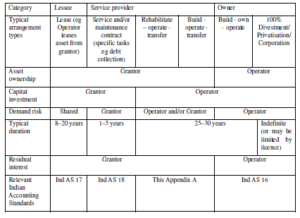

Information note 2

References to Indian Accounting Standards that apply to typical types of public-to-private arrangements

This note accompanies, but is not part of, Appendix A.

The table sets out the typical types of arrangements for private sector participation in the provision of public sector services and provides references to Indian Accounting Standards that apply to those arrangements. The list of arrangements types is not exhaustive. The purpose of the table is to highlight the continuum of arrangements. It is not Appendix A’s intention to convey the impression that bright lines exist between the accounting requirements for public-to- private arrangements

Appendix B

Service Concession Arrangements: Disclosures

This Appendix is an integral part of Indian Accounting Standard (Ind AS) 11.

Issues

1. An entity (the operator) may enter into an arrangement with another entity (the grantor) to provide services that give the public access to major economic and social facilities. The grantor may be a public or private sector entity, including a governmental body. Examples of service concession arrangements involve water treatment and supply facilities, motorways, car parks, tunnels, bridges, airports and telecommunication networks. Examples of arrangements that are not service concession arrangements include an entity outsourcing the operation of its internal services (eg employee cafeteria, building maintenance, and accounting or information technology functions).

2. A service concession arrangement generally involves the grantor conveying for the period of the concession to the operator:

(a) the right to provide services that give the public access to major economic and social facilities, and

(b) in some cases, the right to use specified tangible assets, intangible assets, or financial assets, in exchange for the operator:

(c) committing to provide the services according to certain terms and conditions during the concession period, and

(d) when applicable, committing to return at the end of the concession period the rights received at the beginning of the concession period and/or acquired during the concession period.

3. The common characteristic of all service concession arrangements is that the operator both receives a right and incurs an obligation to provide public services.

4. The issue is what information should be disclosed in the notes in the financial statements of an operator and a grantor.

5. Certain aspects and disclosures relating to some service concession arrangements are addressed by Indian Accounting Standards (eg Ind AS 16 applies to acquisitions of items of property, plant and equipment, Ind AS 17 applies to leases of assets, and Ind AS 38 applies to acquisitions of intangible assets). However, a service concession arrangement may involve executory contracts that are not addressed in Indian Accounting Standards, unless the contracts are onerous, in which case Ind AS 37 applies. Therefore, this Appendix addresses additional disclosures of service concession arrangements.

Accounting Principles

6. All aspects of a service concession arrangement shall be considered in determining the appropriate disclosures in the notes. An operator and a grantor shall disclose the following in each period:

(a) a description of the arrangement;

(b) significant terms of the arrangement that may affect the amount, timing and certainty of future cash flows (eg the period of the concession, re-pricing dates and the basis upon which re-pricing or re-negotiation is determined);

(c) the nature and extent (eg quantity, time period or amount as appropriate) of:

(i) rights to use specified assets;

(ii) obligations to provide or rights to expect provision of services;

(iii) obligations to acquire or build items of property, plant and equipment;

(iv) obligations to deliver or rights to receive specified assets at the end of the concession period;

(v) renewal and termination options; and

(vi) other rights and obligations (eg major overhauls);

(d) changes in the arrangement occurring during the period; and

(d) how the service arrangement has been classified.

6A An operator shall disclose the amount of revenue and profits or losses recognized in the period on exchanging construction services for a financial asset or an intangible asset.

7 The disclosures required in accordance with paragraph 6 of this Appendix shall be provided individually for each service concession arrangement or in aggregate for each class of service concession arrangements. A class is a grouping of service concession arrangements involving services of a similar nature (eg toll collections, telecommunications and water treatment services).

Appendix C

References to matters contained in other Indian Accounting Standards

This Appendix is an integral part of Indian Accounting Standard (Ind AS) 11.

This appendix lists the appendices which are part of other Indian Accounting Standards and makes reference to Ind AS 11, Construction Contracts.

1. Appendix A Intangible Assets—Web Site Costs contained in Ind AS 38, Intangible Assets.

Appendix 1

Note: This Appendix is not a part of the Indian Accounting Standard. The purpose of this Appendix is only to bring out the differences, if any, between Indian Accounting Standard (Ind AS) 11 and the corresponding International Accounting Standard (IAS) 11, Construction Contracts, IFRIC 12, Service Concession Arrangements and SIC 29, Service Concession Arrangements: Disclosures

Comparison with IAS 11, Construction Contracts, IFRIC 12, Service Concession

Arrangements and SIC 29, Service Concession Arrangements: Disclosures

1. The transitional provisions given in IFRIC 12 have not been given in Ind AS 11, since all transitional provisions related to Ind ASs, wherever considered appropriate have been included in Ind AS 101, First-time Adoption of Indian Accounting Standards corresponding to IFRS 1, First-time Adoption of International Financial Reporting Standards.

2. Different terminology is used in this standard, e.g., the term ‘balance sheet’ is used instead of ‘Statement of financial position’ and ‘Statement of profit and loss’ is used instead of ‘Statement of comprehensive income’.

3. Paragraph 2 of IAS 11 which states that IAS 11 supersedes the earlier version of IAS 11 is deleted in Ind AS 11 as this is not relevant in Ind AS 11. However, paragraph number 2 is retained in Ind AS 11 to maintain consistency with paragraph numbers of IAS 11.’’.

Omitted vide Companies (Indian Accounting Standards) Amendment Rules, 2018 dated 28th March,2018 effective from 01st April,2018.

Inserted vide Companies (Indian Accounting Standards) (Amendment) Rules, 2016, GSR 365(E) dated 30.03.2016. To view the notification,Click Here

Companies (Indian Accounting Standards) (Amendment) Rules, 2016 [GSR 365(E)] dated 30/03/2016

The Companies (Indian Accounting Standards) Amendment Rules, 2018 dated 28.03.2018 w.e.f., 01.04.2018