Regulation 48 of LODR

The Central Government the standards of accounting or any addendum thereto, as recommended by the Institute of Chartered Accountants of India, constituted under section 3 of the Chartered Accountants Act, 1949, in consultation with and after examination of the recommendations made by the National Financial Reporting Authority.

that until the National financial Reporting Authority is constituted under section 132 of the Companies Act, 2013 (18 of 2013), the standards of accounting or any addendum there to as recommended by the Institute of Chartered Accountants of India constituted under section 3 of the Chartered Accountants Act. 1949 (18 of 1949) in consultation with and after examination or the recommendations made by National Advisory Committee on Accounting Standards constituted under section 210 A of the Companies Act, I956. (Effective from 1st April,2015)

- MCA has notified The Companies (Accounting Standards) Rules, 2021. To view the rules,Click Here

- All Regional Directors and Registrar of Companies are instructed by MCA that till the Standards of Accounting or any addendum thereto are prescribed by Central Government in consultation and recommendation of the National Financial Reporting Authority, the existing Accounting Standards notified under the Companies Act, 1956 shall continue to apply vide General Circular 15/2013. To view the clarification,Click Here

9.1.7-Companies (Accounts) Rules,2014

7. Transitional provisions with respect to Accounting Standards.-

(1) The standards of accounting as specified under the Companies Act, 1956 (1 of 1956) shall be deemed to be the accounting standards until accounting standards are specified by the Central Government under section 133.

(2) Till the National Financial Reporting Authority is constituted under section 132 of the Act, the Central Government may prescribe the standards of accounting or any addendum thereto, as recommended by the Institute of Chartered Accountants of India in consultation with and after examination of the recommendations made by the National Advisory Committee on Accounting Standards constituted under section 210A of the Companies Act, 1956 (1 of 1956).

9.3.1- Companies (Indian Accounting Standards) Rules, 2015

9.3.2- Companies (Indian Accounting Standards) Rules, 2015

9.3.3- Companies (Indian Accounting Standards) Rules, 2015

9.3.4- Companies (Indian Accounting Standards) Rules, 2015

9.3.5- Companies (Indian Accounting Standards) Rules, 2015

The insurance companies, banking companies and non-banking finance companies shall not be required to apply Indian Accounting Standards (Ind AS) for preparation of their financial statements either voluntarily or mandatorily as specified in sub-rule (1) of rule 4.

an insurer or insurance company may provide its financial statement as per Ind AS 104 for the purposes of consolidated financial statements by its parent or investor or venturer till the Insurance Regulatory and Development Authority notifies the Ind AS 117 and for this purpose, Ind AS 104 shall, as specified in the Schedule to these rules, continue to apply.

9.9.1- Companies (Accounting Standards) Rules, 2021

1. Short title and commencement.-

(1) These rules may be called the Companies (Accounting Standards) Rules, 2021.

(2) They shall come into force on the date of their publication in the Official Gazette.

9.9.2- Companies (Accounting Standards) Rules, 2021

2.Definitions.-

(1) In these rules, unless the context otherwise requires,-

(a) “Accounting Standards” means the standards of accounting or any addendum thereto as specified in rule 3;

(b) “Act” means the Companies Act, 2013 (18 of 2013);

(c)“Annexure” in relation to these rules means the Annexure containing the Accounting Standards (AS) appended to these rules;

(d)“Enterprise” means a ‘company’ as defined in clause(20) of section 2 of the Act;

(e) “Small and Medium Sized Company” (SMC) means, a company-

(i) whose equity or debt securities are not listed or are not in the process of listing on any stock exchange, whether in India or outside India;

(ii) which is not a bank, financial institution or an insurance company;

(iii) whose turnover (excluding other income) does not exceed two hundred and fifty crore rupees in the immediately preceding accounting year;

(iv) which does not have borrowings (including public deposits) in excess of fifty crore rupees at any time during the immediately preceding accounting year; and

(v) which is not a holding or subsidiary company of a company which is not a small and medium-sized company.

Explanation.-For the purposes of this clause, a company shall qualify as a Small and Medium Sized Company, if the conditions mentioned therein are satisfied as at the end of the relevant accounting period.

(2) Words and expressions used and not defined in these rules but defined in the Act shall have the meanings respectively assigned to them in the Act.

9.9.3- Companies (Accounting Standards) Rules, 2021

3. Accounting Standards.-

(1) The Central Government hereby specifies Accounting Standards 1 to 5, 7and 9 to 29 as recommended by the Institute of Chartered Accountants of India, which are specified in the to these rules.

(2) The Accounting Standards shall come into effect in respect of accounting periods commencing on or after the 1stday of April, 2021.

9.9.4- Companies (Accounting Standards) Rules, 2021

4. Obligation to comply with Accounting Standards.-

(1) Every company, other than companies on which Indian Accounting Standards as notified under Companies (Indian Accounting Standards) Rules, 2015 are applicable, and its auditor(s)shall comply with the Accounting Standards in the manner specified in the Annexure.

(2) The Accounting Standards shall be applied in the preparation of Financial Statements

9.9.5- Companies (Accounting Standards) Rules, 2021

5. Qualification for exemption or relaxation in respect of SMC:-

An existing company, which was previously not Small and Medium Sized Company (SMC) and subsequently becomes a SMC, shall not be qualified for exemption or relaxation in respect of Accounting Standards available to a SMC until the company remains a SMC for two consecutive accounting periods.

Indian Accounting Standard (Ind AS) 1

Presentation of Financial Statements

(This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority.

Paragraphs in bold type indicate the main principles).

Objective

1 This Standard prescribes the basis for presentation of general purpose financial statements to ensure comparability both with the entity’s financial statements of previous periods and with the financial statements of other entities. It sets out overall requirements for the presentation of financial statements, guidelines for their structure and minimum requirements for their content.

Scope

2 An entity shall apply this Standard in preparing and presenting general purpose financial statements in accordance with Indian Accounting Standards (Ind ASs).

3 Other Ind ASs set out the recognition, measurement and disclosure requirements for specific transactions and other events.

4 This Standard does not apply to the structure and content of condensed interim financial statements prepared in accordance with Ind AS 34, Interim Financial Reporting. However, paragraphs 15–35 apply to such financial statements. This Standard applies equally to all entities, including those that present consolidated financial statements in accordance with Ind AS 110, Consolidated Financial Statements, and those that present separate financial statements in accordance with Ind AS 27, Separate Financial Statements.

5 This Standard uses terminology that is suitable for profit-oriented entities, including public sector business entities. If entities with not-for-profit activities in the private sector or the public sector apply this Standard, they may need to amend the descriptions used for particular line items in the financial statements and for the financial statements themselves.

6 Similarly, entities whose share capital is not equity may need to adapt the financial statement presentation of members’ interests.

Definitions

7 The following terms are used in this Standard with the meanings specified:

General purpose financial statements (referred to as ‘financial statements’) are those intended to meet the needs of users who are not in a position to require an entity to prepare reports tailored to their particular information needs.

Impracticable Applying a requirement is impracticable when the entity cannot apply it after making every reasonable effort to do so.

Indian Accounting Standards (Ind ASs) are Standards prescribed under Section 133 of the Companies Act, 2013.

Information is material if omitting, misstating or obscuring it could reasonably be expected to influence decisions that the primary users of general purpose financial statements make on the basis of those financial statements, which provide financial information about a specific reporting entity.

Materiality depends on the nature or magnitude of information, or both. An entity assesses whether information, either individually or in combination with other information, is material in the context of its financial statements taken as a whole.

Information is obscured if it is communicated in a way that would have a similar effect for primary users of financial statements to omitting or misstating that information. The following are examples of circumstances that may result in material information being obscured:-

(a) information regarding a material item, transaction or other event is disclosed in the financial statements but the language used is vague or unclear;

(b) information regarding a material item, transaction or other event is scattered throughout the financial statements;

(c) dissimilar items, transactions or other events are inappropriately aggregated;

(d) similar items, transactions or other events are inappropriately disaggregated; and

(e) the understandability of the financial statements is reduced as a result of material information being hidden by immaterial information to the extent that a primary user is unable to determine what information is material.

Assessing whether information could reasonably be expected to influence decisions made by the primary users of a specific reporting entity‘s general purpose financial statements requires an entity to consider the characteristics of those users while also considering the entity‘s own circumstances.

Many existing and potential investors, lenders and other creditors cannot require reporting entities to provide information directly to them and must rely on general purpose financial statements for much of the financial information they need. Consequently, they are the primary users to whom general purpose financial statements are directed. Financial statements are prepared for users who have a reasonable knowledge of business and economic activities and who review and analyse the information diligently. At times, even well informed and diligent users may need to seek the aid of an adviser to understand information about complex economic phenomena.

Material Omissions or misstatements of items are material if they could, individually or collectively, influence the economic decisions that users make on the basis of the financial statements. Materiality depends on the size and nature of the omission or misstatement judged in the surrounding circumstances. The size or nature of the item, or a combination of both, could be the determining factor.

Assessing whether an omission or misstatement could influence economic decisions of users, and so be material, requires consideration of the characteristics of those users. The Framework for the Preparation and Presentation of Financial Statements issued by the Institute of Chartered Accountants of India states in paragraph 25 that ‘users are assumed to have a reasonable knowledge of business and economic activities and accounting and a willingness to study the information with reasonable diligence.’ Therefore, the assessment needs to take into account how users with such attributes could reasonably be expected to be influenced in making economic decisions.

Notes contain information in addition to that presented in the balance sheet ), statement of profit and loss, statement of changes in equity and statement of cash flows. Notes provide narrative descriptions or disaggregations of items presented in those statements and information about items that do not qualify for recognition in those statements.

Other comprehensive income comprises items of income and expense (including reclassification adjustments) that are not recognised in profit or loss as required or permitted by other Ind ASs.

The components of other comprehensive income include:

(a) changes in revaluation surplus (see Ind AS 16, Property, Plant and Equipment and Ind AS 38, Intangible Assets);

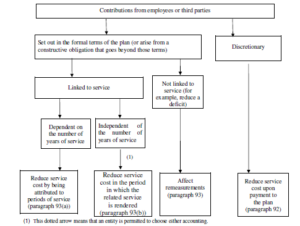

(b) reameasurements of defined benefit plans (see Ind AS 19, Employee Benefits);

(c) gains and losses arising from translating the financial statements of a foreign operation (see Ind AS 21, The Effects of Changes in Foreign Exchange Rates);

(d) gains and losses from investments in equity instruments designated at fair value through other comprehensive income in accordance with paragraph 5.7.5 of Ind AS 109, Financial Instruments;

(da) gains and losseson financial assets measured at fair value through other comprehensive income in accordance with paragraph 4.1.2A of Ind AS 109.

(e) the effective portion of gains and losses on hedging instruments in a cash flow hedge and the gains and losses on hedging instruments that hedge investments in equity instruments measured at fair value through other comprehensive income in accordance with paragraph 5.7.5 of Ind AS 109 (see Chapter 6 of Ind AS 109);

(f) for particular liabilities designated as at fair value through profit or loss, the amount of the change in fair value that is attributable to changes in the liability’s credit risk (see paragraph 5.7.7 of Ind AS 109);

(g) changes in the value of the time value of options when separating the intrinsic value and time value of an option contract and designating as the hedging instrument only the changes in the intrinsic value (see Chapter 6 of Ind AS 109);

changes in the value of the forward elements of forward contracts when separating the forward element and spot element of a forward contract and designating as the hedging instrument only the changes in the spot element, and changes in the value of the foreign currency basis spread of a financial instrument when excluding it from the designation of that financial instrument as the hedging instrument (see Chapter 6 of Ind AS 109);

insurance finance income and expenses from contracts issued within the scope of Ind AS 117, Insurance Contracts, excluded from profit or loss when total insurance finance income or expenses is disaggregated to include in profit or loss an amount determined by a systematic allocation applying paragraph 88(b) of Ind AS 117, or by an amount that eliminates accounting mismatches with the finance income or expenses arising on the underlying items, applying paragraph 89(b) of Ind AS 117; and

finance income and expenses reinsurance contracts held excluded from profit or loss when total reinsurance finance or expenses is disaggregated to include in profit or loss an amount determined by a systematic allocation applying paragraph 88(b) of Ind AS 117.

(h) changes in the value of the forward elements of forward contracts when separating the forward element and spot element of a forward contract and designating as the hedging instrument only the changes in the spot element, and changes in the value of the foreign currency basis spread of a financial instrument when excluding it from the designation of that financial instrument as the hedging instrument (see Chapter 6 of Ind AS 109).

Owners are holders of instruments classified as equity.

Profit or loss is the total of income less expenses, excluding the components of other comprehensive income.

Reclassification adjustments are amounts reclassified to profit or loss in the current period that were recognised in other comprehensive income in the current or previous periods.

Total comprehensive income is the change in equity during a period resulting from transactions and other events, other than those changes resulting from transactions with owners in their capacity as owners.

Total comprehensive income comprises all components of ‘profit or loss’ and of ‘other comprehensive income’.

8 [Refer Appendix 1]

8A The following terms are described in Ind AS 32, Financial Instruments: Presentation, and are used in this Standard with the meaning specified in Ind AS 32:

(a) puttable financial instrument classified as an equity instrument (described in paragraphs 16A and 16B of Ind AS 32)

(b) an instrument that imposes on the entity an obligation to deliver to another party a pro rata share of the net assets of the entity only on liquidation and is classified as an equity instrument (described in paragraphs 16C and 16D of Ind AS 32).

Financial statements

Purpose of financial statements

9 Financial statements are a structured representation of the financial position and financial performance of an entity. The objective of financial statements is to provide information about the financial position, financial performance and cash flows of an entity that is useful to a wide range of users in making economic decisions. Financial statements also show the results of the management’s stewardship of the resources entrusted to it. To meet this objective, financial statements provide information about an entity’s:

(a) assets;

(b) liabilities;

(c) equity;

(d) income and expenses, including gains and losses;

(e) contributions by and distributions to owners in their capacity as owners; and

(f) cash flows.

This information, along with other information in the notes, assists users of financial statements in predicting the entity’s future cash flows and, in particular, their timing and certainty.

Complete set of financial statements

10 A complete set of financial statements comprises:

(a) a balance sheet as at the end of the period ;

(b) a statement of profit and loss for the period;

(c) Statement of changes in equity for the period;

(d) a statement of cash flows for the period;

(e) notes, comprising a summary of significant accounting policies and other explanatory information; and

notes, comprising significant accounting policies and other explanatory information;

(ea) comparative information in respect of the preceding period as specified in paragraphs 38 and 38A; and

(f) a balance sheet as at the beginning of the preceding period when an entity applies an accounting policy retrospectively or makes a retrospective restatement of items in its financial statements, or when it reclassifies items in its financial statements in accordance with paragraphs 40A–40D.

10A An entity shall present a single statement of profit and loss, with profit or loss and other comprehensive income presented in two sections. The sections shall be presented together, with the profit or loss section presented first followed directly by the other comprehensive income section.

11 An entity shall present with equal prominence all of the financial statements in a complete set of financial statements.

12 [Refer Appendix 1]

13 Many entities present, outside the financial statements, a financial review by management that describes and explains the main features of the entity’s financial performance and financial position, and the principal uncertainties it faces. Such a report may include a review of:

(a) the main factors and influences determining financial performance, including changes in the environment in which the entity operates, the entity’s response to those changes and their effect, and the entity’s policy for investment to maintain and enhance financial performance, including its dividend policy;

(b) the entity’s sources of funding and its targeted ratio of liabilities to equity; and

(c) the entity’s resources not recognised in the balance sheet in accordance with Ind ASs.

14 Many entities also present, outside the financial statements, reports and statements such as environmental reports and value added statements, particularly in industries in which environmental factors are significant and when employees are regarded as an important user group. Reports and statements presented outside financial statements are outside the scope of Ind ASs.

General features

Presentation of True and Fair View and compliance with Ind ASs

15 Financial statements shall present a true and fair view of the financial position, financial performance and cash flows of an entity. Presentation of true and fair view requires the faithful representation of the effects of transactions, other events and conditions in accordance with the definitions and recognition criteria for assets, liabilities, income and expenses set out in the Framework. The application of Ind ASs, with additional disclosure when necessary, is presumed to result in financial statements that present a true and fair view.

16 An entity whose financial statements comply with Ind ASs shall make an explicit and unreserved statement of such compliance in the notes. An entity shall not describe financial statements as complying with Ind ASs unless they comply with all the requirements of Ind ASs.

17 In virtually all circumstances, presentation of a true and fair view is achieved by compliance with applicable Ind ASs. Presentation of a true and fair view also requires an entity:

(a) to select and apply accounting policies in accordance with Ind AS 8, Accounting Policies, Changes in Accounting Estimates and Errors. Ind AS 8 sets out a hierarchy of authoritative guidance that management considers in the absence of an Ind AS that specifically applies to an item.

(b) to present information, including accounting policies, in a manner that provides relevant, reliable, comparable and understandable information.

(c) to provide additional disclosures when compliance with the specific requirements in Ind ASs is insufficient to enable users to understand the impact of particular transactions, other events and conditions on the entity’s financial position and financial performance.

18 An entity cannot rectify inappropriate accounting policies either by disclosure of the accounting policies used or by notes or explanatory material.

19 In the extremely rare circumstances in which management concludes that compliance with a requirement in an Ind AS would be so misleading that it would conflict with the objective of financial statements set out in the Framework, the entity shall depart from that requirement in the manner set out in paragraph 20 if the relevant regulatory framework requires, or otherwise does not prohibit, such a departure.

20 When an entity departs from a requirement of an Ind AS in accordance with paragraph 19, it shall disclose:

(a) that management has concluded that the financial statements present a true and fair view of the entity’s financial position, financial performance and cash flows;

(b) that it has complied with applicable Ind ASs, except that it has departed from a particular requirement to present a true and fair view;

(c) the title of the Ind AS from which the entity has departed, the nature of the departure, including the treatment that the Ind AS would require, the reason why that treatment would be so misleading in the circumstances that it would conflict with the objective of financial statements set out in the Framework, and the treatment adopted; and

(d) for each period presented, the financial effect of the departure on each item in the financial statements that would have been reported in complying with the requirement.

21 When an entity has departed from a requirement of an Ind AS in a prior period, and that departure affects the amounts recognised in the financial statements for the current period, it shall make the disclosures set out in paragraph 20(c) and (d).

22 Paragraph 21 applies, for example, when an entity departed in a prior period from a requirement in an Ind AS for the measurement of assets or liabilities and that departure affects the measurement of changes in assets and liabilities recognised in the current period’s financial statements.

23 In the extremely rare circumstances in which management concludes that compliance with a requirement in an Ind AS would be so misleading that it would conflict with the objective of financial statements set out in the Framework, but the relevant regulatory framework prohibits departure from the requirement, the entity shall, to the maximum extent possible, reduce the perceived misleading aspects of compliance by disclosing:

(a) the title of the Ind AS in question, the nature of the requirement, and the reason why management has concluded that complying with that requirement is so misleading in the circumstances that it conflicts with the objective of financial statements set out in the Framework; and

(b) for each period presented, the adjustments to each item in the financial statements that management has concluded would be necessary to present a true and fair view.

24 For the purpose of paragraphs 19–23, an item of information would conflict with the objective of financial statements when it does not represent faithfully the transactions, other events and conditions that it either purports to represent or could reasonably be expected to represent and, consequently, it would be likely to influence economic decisions made by users of financial statements. When assessing whether complying with

a specific requirement in an Ind AS would be so misleading that it would conflict with the objective of financial statements set out in the Framework, management considers:

(a) why the objective of financial statements is not achieved in the particular circumstances; and

(b) how the entity’s circumstances differ from those of other entities that comply with the requirement. If other entities in similar circumstances comply with the requirement, there is a rebuttable presumption that the entity’s compliance with the requirement would not be so misleading that it would conflict with the objective of financial statements set out in the Framework.

Going concern

25 When preparing financial statements, management shall make an assessment of an entity’s ability to continue as a going concern. An entity shall prepare financial statements on a going concern basis unless management either intends to liquidate the entity or to cease trading, or has no realistic alternative but to do so. When management is aware, in making its assessment, of material uncertainties related to events or conditions that may cast significant doubt upon the entity’s ability to

continue as a going concern, the entity shall disclose those uncertainties. When an entity does not prepare financial statements on a going concern basis, it shall disclose that fact, together with the basis on which it prepared the financial statements and the reason why the entity is not regarded as a going

concern.

26 In assessing whether the going concern assumption is appropriate, management takes into account all available information about the future, which is at least, but is not limited to, twelve months from the end of the reporting period. The degree of consideration depends on the facts in each case. When an entity has a history of profitable operations and ready access to financial resources, the entity may reach a conclusion that

the going concern basis of accounting is appropriate without detailed analysis. In other cases, management may need to consider a wide range of factors relating to current and expected profitability, debt repayment schedules and potential sources of replacement financing before it can satisfy itself that the going concern basis is appropriate.

Accrual basis of accounting

27 An entity shall prepare its financial statements, except for cash flow information, using the accrual basis of accounting.

28 When the accrual basis of accounting is used, an entity recognises items as assets, liabilities, equity, income and expenses (the elements of financial statements) when they satisfy the definitions and recognition criteria for those elements in the Framework.

Materiality and aggregation

29 An entity shall present separately each material class of similar items. An entity shall present separately items of a dissimilar nature or function unless they are immaterial except when required by law.

30 Financial statements result from processing large numbers of transactions or other events that are aggregated into classes according to their nature or function. The final stage in the process of aggregation and classification is the presentation of condensed and classified data, which form line items in the financial statements. If a line item is not individually material, it is aggregated with other items either in those statements or in the notes. An item that is not sufficiently material to warrant separate presentation in those

statements may warrant separate presentation in the notes.

When applying this and other Ind ASs an entity shall decide, taking into consideration all relevant facts and circumstances, how it aggregates information in the financial statements, which include the notes. An entity shall not reduce the understandability of its financial statements by obscuring material information with immaterial information or by aggregating material items that have different natures or functions.

31 An entity need not provide a specific disclosure required by an Ind AS if the information is not material except when required by law.

Some Ind ASs specify information that is required to be included in the financial statements, which include the notes. An entity need not provide a specific disclosure required by an Ind AS if the information resulting from that disclosure is not material except when required by law. This is the case even if the Ind AS contains a list of specific requirements or describes them as minimum requirements. An entity shall also consider whether to provide additional disclosures when compliance with the specific requirements in Ind AS is insufficient to enable users of financial statements to understand the impact of particular transactions, other events and conditions on the entity’s financial position and financial performance.

Offsetting

32 An entity shall not offset assets and liabilities or income and expenses, unless required or permitted by an Ind AS.

33 An entity reports separately both assets and liabilities, and income and expenses. Offsetting in the statement of profit and loss or balance sheet, except when offsetting reflects the substance of the transaction or other event, detracts from the ability of users both to understand the transactions, other events and conditions that have occurred and to assess the entity’s future cash flows. Measuring assets net of valuation allowances—for

example, obsolescence allowances on inventories and doubtful debts allowances on receivables—is not offsetting.

Ind AS 115, Revenue from Contracts with Customers, requires an entity to measure revenue from contracts with customers at the amount of consideration to which the entity expects to be entitled in exchange for transferring promised goods or services. For example, the amount of revenue recognized reflects any trade discounts and volume rebates the entity allows. An entity undertakes, in the course of its ordinary activities, other transactions that do not generate revenue but are incidental to the main revenue-generating activities. An entity presents the results of such transactions, when this presentation reflects the substance of the transaction or other event, by netting any income with related expenses arising on the same transaction. For example:

(a) an entity presents gains and losses on the disposal of non-current assets, including investments and operating assets, by deducting from the amount of consideration on disposal the carrying amount of the asset and related selling expenses; and

(b) an entity may net expenditure related to a provision that is recognised in accordance with Ind AS 37, Provisions, Contingent Liabilities and Contingent Assets, and reimbursed under a contractual arrangement with a third party (for example, a supplier’s warranty agreement) against the related reimbursement.

34 Ind AS 115, Revenue from Contracts with Customers requires an entity to measure revenue from contracts with customers at the amount of consideration to which the entity expects to be entitled in exchange for transferring promised goods or services. For example, the amount of revenue recognised reflects any trade discounts and volume rebates the entity allows. An entity undertakes, in the course of its ordinary activities,

other transactions that do not generate revenue but are incidental to the main revenue-generating activities. An entity presents the results of such transactions, when this presentation reflects the substance of the transaction or other event, by netting any income with related expenses arising on the same transaction. For example:

(a) an entity presents gains and losses on the disposal of non-current assets, including investments and operating assets, by deducting from the amount of consideration on disposal the carrying amount of the asset and related selling expenses; and

(b) an entity may net expenditure related to a provision that is recognised in accordance with Ind AS 37, Provisions, Contingent Liabilities and Contingent Assets, and reimbursed under a contractual arrangement with a third party (for example, a supplier’s warranty agreement) against the related reimbursement.

Ind AS 18, Revenue, defines revenue and requires an entity to measure it at the fair value of the consideration received or receivable, taking into account the amount of any trade discounts and volume rebates the entity allows. An entity undertakes, in the course of its ordinary activities, other transactions that do not generate revenue but are incidental to the main revenue-generating activities. An entity presents the results of such transactions, when this presentation reflects the substance of the transaction or other event, by netting any income with related expenses arising on the same transaction.

For example:

(a) an entity presents gains and losses on the disposal of non-current assets, including investments and operating assets, by deducting from the proceeds on disposal the carrying amount of the asset and related selling expenses; and

(b) an entity may net expenditure related to a provision that is recognised in accordance with Ind AS 37, Provisions, Contingent Liabilities and Contingent Assets, and reimbursed under a contractual arrangement with a third party (for example, a supplier’s warranty agreement) against the related reimbursement.

35 In addition, an entity presents on a net basis gains and losses arising from a group of similar transactions, for example, foreign exchange gains and losses or gains and losses arising on financial instruments held for trading. However, an entity presents such gains and losses separately if they are material.

Frequency of reporting

36 An entity shall present a complete set of financial statements (including comparative information) at least annually. When an entity changes the end of its reporting period and presents financial statements for a period longer or shorter than one year, an entity shall disclose, in addition to the period covered by the financial statements:

(a) the reason for using a longer or shorter period, and

(b) the fact that amounts presented in the financial statements are not entirely comparable.

37 [Refer Appendix 1]

Comparative information

Minimum comparative information

38 Except when Ind ASs permit or require otherwise, an entity shall present comparative information in respect of the preceding period for all amounts reported in the current period’s financial statements. An entity shall include comparative information for narrative and descriptive information if it is relevant to understanding the current period’s financial statements.

38A An entity shall present, as a minimum, two balance sheets , two statements of profit and loss, two statements of cash flows and two statements of changes in equity, and related notes.

38B In some cases, narrative information provided in the financial statements for the preceding period(s) continues to be relevant in the current period. For example, an entity discloses in the current period details of a legal dispute, the outcome of which was uncertain at the end of the preceding period and is yet to be resolved. Users may benefit from the disclosure of information that the uncertainty existed at the end of the preceding

period and from the disclosure of information about the steps that have been taken during the period to resolve the uncertainty.

Additional comparative information

38C An entity may present comparative information in addition to the minimum comparative financial statements required by Ind ASs, as long as that information is prepared in accordance with Ind ASs. This comparative information may consist of one or more statements referred to in paragraph 10, but need not comprise a complete set of financial statements. When this is the case, the entity shall present related note information for those additional statements.

38D For example, an entity may present a third statement of profit and loss (thereby presenting the current period, the preceding period and one additional comparative period). However, the entity is not required to present a third balance sheet, a third statement of cash flows or a third statement of changes in equity (ie an additional

financial statement comparative). The entity is required to present, in the notes to the financial statements, the comparative information related to that additional statement of profit and loss.

39- [Refer Appendix 1]

40

Change in accounting policy, retrospective restatement or reclassification

40A An entity shall present a third balance sheet as at the beginning of the preceding period in addition to the minimum comparative financial statements required in paragraph 38A if:

(a) it applies an accounting policy retrospectively, makes a retrospective restatement of items in its financial statements or reclassifies items in its financial statements; and

(b) the retrospective application, retrospective restatement or the reclassification has a material effect on the information in the balance sheet at the beginning of the preceding period.

40B In the circumstances described in paragraph 40A, an entity shall present three

balance sheets as at:

(a) the end of the current period;

(b) the end of the preceding period; and

(c) the beginning of the preceding period.

40C When an entity is required to present an additional balance sheet in accordance with paragraph 40A, it must disclose the information required by paragraphs 41– 44 and Ind AS 8. However, it need not present the related notes to the opening balance sheet as at the beginning of the preceding period.

40D The date of that opening balance sheet shall be as at the beginning of the preceding period regardless of whether an entity’s financial statements present comparative information for earlier periods (as permitted in

paragraph 38C).

41 If an entity changes the presentation or classification of items in its financial statements, it shall reclassify comparative amounts unless reclassification is impracticable. When an entity reclassifies comparative amounts, it shall disclose (including as at the beginning of the preceding period):

(a) the nature of the reclassification;

(b) the amount of each item or class of items that is reclassified; and

(c) the reason for the reclassification.

42 When it is impracticable to reclassify comparative amounts, an entity shall disclose:

(a) the reason for not reclassifying the amounts, and

(b) the nature of the adjustments that would have been made if the amounts had been reclassified.

43 Enhancing the inter-period comparability of information assists users in making economic decisions, especially by allowing the assessment of trends in financial information for predictive purposes. In some circumstances, it is impracticable to reclassify comparative information for a particular prior period to achieve

comparability with the current period. For example, an entity may not have collected data in the prior period(s) in a way that allows reclassification, and it may be impracticable to recreate the information.

44 Ind AS 8 sets out the adjustments to comparative information required when an entity changes an accounting policy or corrects an error.

Consistency of presentation

45 An entity shall retain the presentation and classification of items in the financial statements from one period to the next unless:

(a) it is apparent, following a significant change in the nature of the entity’s operations or a review of its financial statements, that another presentation or classification would be more appropriate having regard to the criteria for the selection and application of accounting policies in Ind AS 8; or

(b) an Ind AS requires a change in presentation.

46 For example, a significant acquisition or disposal, or a review of the presentation of the financial statements, might suggest that the financial statements need to be presented differently. An entity changes the presentation of its financial statements only if the changed presentation provides information that is reliable and more relevant to users of the financial statements and the revised structure is likely to continue, so that

comparability is not impaired. When making such changes in presentation, an entity reclassifies its comparative information in accordance with paragraphs 41 and 42.

Structure and content

Introduction

47 This Standard requires particular disclosures in the balance sheet or in the statement of profit and loss, or in the statement of changes in equity and requires disclosure of other line items either in those statements or in the notes. Ind AS 7, Statement of Cash Flows, sets out requirements for the presentation of cash flow information.

48 This Standard sometimes uses the term ‘disclosure’ in a broad sense, encompassing items presented in the financial statements. Disclosures are also required by other Ind ASs. Unless specified to the contrary elsewhere in this Standard or in another Ind AS, such disclosures may be made in the financial statements.

Identification of the financial statements

49 An entity shall clearly identify the financial statements and distinguish them from other information in the same published document.

50 Ind ASs apply only to financial statements, and not necessarily to other information presented in an annual report, a regulatory filing, or another document. Therefore, it is important that users can distinguish information that is prepared using Ind ASs from other information that may be useful to users but is not the subject of those requirements.

51 An entity shall clearly identify each financial statement and the notes. In addition, an entity shall display the following information prominently, and repeat it when necessary for the information presented to be understandable:

(a) the name of the reporting entity or other means of identification, and any change in that information from the end of the preceding reporting period;

(b) whether the financial statements are of an individual entity or a group of entities;

(c) the date of the end of the reporting period or the period covered by the set of financial statements or notes;

(d) the presentation currency, as defined in Ind AS 21; and

(e) the level of rounding used in presenting amounts in the financial statements.

52 An entity meets the requirements in paragraph 51 by presenting appropriate headings for pages, statements, notes, columns and the like. Judgement is required in determining the best way of presenting such information. For example, when an entity presents the financial statements electronically, separate pages are not always used; an entity then presents the above items to ensure that the information included in the financial statements can be understood.

53 An entity often makes financial statements more understandable by presenting information in thousands, lakhs, millions or crores of units of the presentation currency. This is acceptable as long as the entity discloses the level of rounding and does not omit material information.

Balance Sheet

Information to be presented in the balance sheet

54 As a minimum, the balance sheet shall include line items that present the following amounts :

The balance sheet shall include line items that present the following amounts:

(a) property, plant and equipment;

(b) investment property;

(c) intangible assets;

(d) financial assets [excluding amounts shown under (e), (h) and (i)];

portfolios of contracts within the scope of Ind AS 117 that are assets, disaggregated as required by paragraph 78 of Ind AS 117;

(e) investments accounted for using the equity method;

(f) biological assets within the scope of Ind AS 41 Agriculture;

(g) inventories;

(h) trade and other receivables;

(i) cash and cash equivalents;

(j) the total of assets classified as held for sale and assets included in disposal groups classified as held for sale in accordance with Ind AS 105, Non-current Assets Held for Sale and Discontinued Operations;

(k) trade and other payables;

(l) provisions;

(m) financial liabilities (excluding amounts shown under (k) and (l));

portfolios of contracts within the scope of Ind AS 117 that are liabilities, disaggregated as required by paragraph 78 of Ind AS 117;

(n) liabilities and assets for current tax, as defined in Ind AS 12, Income Taxes;

(o) deferred tax liabilities and deferred tax assets, as defined in Ind AS 12;

(p) liabilities included in disposal groups classified as held for sale in accordance with Ind AS 105;

(q) non-controlling interests, presented within equity; and

(r) issued capital and reserves attributable to owners of the parent.

55 An entity shall present additional line items, headings and subtotals in the balance sheet when such presentation is relevant to an understanding of the entity’s financial position.

An entity shall present additional line items (including by disaggregating the line items listed in paragraph 54), headings and subtotals in the balance sheet when such presentation is relevant to an understanding of the entity’s financial position.

When an entity presents subtotals in accordance with paragraph 55, those subtotals shall:

(a) be comprised of line items made up of amounts recognised and measured in accordance with Ind AS;

(b) be presented and labelled in a manner that makes the line items that constitute the subtotal clear and understandable;

(c) be consistent from period to period, in accordance with paragraph 45; and

(d) not be displayed with more prominence than the subtotals and totals required in Ind AS for the balance sheet.

56 When an entity presents current and non-current assets, and current and non-current liabilities, as separate classifications in its balance sheet, it shall not classify deferred tax assets (liabilities) as current assets (liabilities).

57 This Standard does not prescribe the order or format in which an entity presents items. Paragraph 54 simply lists items that are sufficiently different in nature or function to warrant separate presentation in the balance sheet. In addition:

(a) line items are included when the size, nature or function of an item or aggregation of similar items is such that separate presentation is relevant to an understanding of the entity’s financial position; and

(b) the descriptions used and the ordering of items or aggregation of similar items may be amended according to the nature of the entity and its transactions, to provide information that is relevant to an understanding of the entity’s financial position. For example, a financial institution may amend the above descriptions to provide information that is relevant to the operations of a financial institution.

58 An entity makes the judgement about whether to present additional items separately on the basis of an assessment of:

(a) the nature and liquidity of assets;

(b) the function of assets within the entity; and

(c) the amounts, nature and timing of liabilities.

59 The use of different measurement bases for different classes of assets suggests that their nature or function differs and, therefore, that an entity presents them as separate line items. For example, different classes of property, plant and equipment can be carried at cost or at revalued amounts in accordance with Ind AS 16.

Current/non-current distinction

60 An entity shall present current and non-current assets, and current and non-current liabilities, as separate classifications in its balance sheet in accordance with paragraphs 66–76 except when a presentation based on liquidity provides information that is reliable and more relevant. When that exception applies, an entity shall present all assets and liabilities in order of liquidity.

61 Whichever method of presentation is adopted, an entity shall disclose the amount expected to be recovered or settled after more than twelve months for each asset and liability line item that combines amounts expected to be recovered or settled:

(a) no more than twelve months after the reporting period, and

(b) more than twelve months after the reporting period.

62 When an entity supplies goods or services within a clearly identifiable operating cycle, separate classification of current and non-current assets and liabilities in the balance sheet provides useful information by distinguishing the net assets that are continuously circulating as working capital from those used in the entity’s long-term operations. It also highlights assets that are expected to be realised within the current operating cycle, and liabilities that are due for settlement within the same period.

63 For some entities, such as financial institutions, a presentation of assets and liabilities in increasing or decreasing order of liquidity provides information that is reliable and more relevant than a current/non-current presentation because the entity does not supply goods or services within a clearly identifiable operating cycle.

64 In applying paragraph 60, an entity is permitted to present some of its assets and liabilities using a current/non-current classification and others in order of liquidity when this provides information that is reliable and more relevant. The need for a mixed basis of presentation might arise when an entity has diverse operations.

65 Information about expected dates of realisation of assets and liabilities is useful in assessing the liquidity and solvency of an entity. Ind AS 107, Financial Instruments: Disclosures, requires disclosure of the maturity dates of financial assets and financial liabilities. Financial assets include trade and other receivables, and financial liabilities include trade and other payables. Information on the expected date of recovery of nonmonetary assets such as inventories and expected date of settlement for liabilities such as provisions is also useful, whether assets and liabilities are classified as current or as non-current. For example, an entity discloses the amount of inventories that are expected to be recovered more than twelve months after the reporting period.

Current assets

66 An entity shall classify an asset as current when:

(a) it expects to realise the asset, or intends to sell or consume it, in its normal operating cycle;

(b) it holds the asset primarily for the purpose of trading;

(c) it expects to realise the asset within twelve months after the reporting period; or

(d) the asset is cash or a cash equivalent (as defined in Ind AS 7) unless the asset is restricted from being exchanged or used to settle a liability for at least twelve months after the reporting period. (d)

An entity shall classify all other assets as non-current.

67 This Standard uses the term ‘non-current’ to include tangible, intangible and financial assets of a long-term nature. It does not prohibit the use of alternative descriptions as long as the meaning is clear.

68 The operating cycle of an entity is the time between the acquisition of assets for processing and their realisation in cash or cash equivalents. When the entity’s normal operating cycle is not clearly identifiable, it is assumed to be twelve months. Current assets include assets (such as inventories and trade receivables) that are sold, consumed or realised as part of the normal operating cycle even when they are not expected to be

realised within twelve months after the reporting period. Current assets also include assets held primarily for the purpose of trading (examples include some financial assets that meet the definition of held for trading in Ind AS 109) and the current portion of non-current financial assets.

Current liabilities

69 An entity shall classify a liability as current when:

(a) it expects to settle the liability in its normal operating cycle;

(b) it holds the liability primarily for the purpose of trading;

(c) the liability is due to be settled within twelve months after the reporting period; or

(d) it does not have an unconditional right to defer settlement of the liability for at least twelve months after the reporting period (see paragraph 73). Terms of a liability that could, at the option of the counterparty, result in its settlement by the issue of equity instruments do not affect its classification

An entity shall classify all other liabilities as non-current.

70 Some current liabilities, such as trade payables and some accruals for employee and other operating costs, are part of the working capital used in the entity’s normal operating cycle. An entity classifies such operating items as current liabilities even if they are due to be settled more than twelve months after the reporting period. The same normal operating cycle applies to the classification of an entity’s assets and liabilities. When

the entity’s normal operating cycle is not clearly identifiable, it is assumed to be twelve months.

71 Other current liabilities are not settled as part of the normal operating cycle, but are due for settlement within twelve months after the reporting period or held primarily for the purpose of trading. Examples are some financial liabilities that meet the definition of held for trading in Ind AS 109, bank overdrafts, and the current portion of non-current financial liabilities, dividends payable, income taxes and other non-trade payables.

Financial liabilities that provide financing on a long-term basis (ie are not part of the working capital used in the entity’s normal operating cycle) and are not due for settlement within twelve months after the reporting period are non-current liabilities, subject to paragraphs 74 and 75.

72 An entity classifies its financial liabilities as current when they are due to be settled within twelve months after the reporting period, even if:

(a) the original term was for a period longer than twelve months, and

(b) an agreement to refinance, or to reschedule payments, on a long-term basis is completed after the reporting period and before the financial statements are approved for issue.

73 If an entity expects, and has the discretion, to refinance or roll over an obligation for at least twelve months after the reporting period under an existing loan facility, it classifies the obligation as non-current, even if it would otherwise be due within a shorter period. However, when refinancing or rolling over the obligation is not at the discretion of the entity (for example, there is no arrangement for refinancing), the entity does not

consider the potential to refinance the obligation and classifies the obligation as current.

74 Where there is a breach of a material provision of a long-term loan arrangement on or before the end of the reporting period with the effect that the liability becomes payable on demand on the reporting date, the entity does not classify the liability as current, if the lender agreed, after the reporting period and before the approval of the financial statements for issue, not to demand payment as a consequence of the breach.

75 However, an entity classifies the liability as non-current if the lender agreed by the end of the reporting period to provide a period of grace ending at least twelve months after the reporting period, within which the entity can rectify the breach and during which the lender cannot demand immediate repayment.

76 [Refer Appendix 1]

Information to be presented either in the balance sheet or in the notes

77 An entity shall disclose, either in the balance sheet or in the notes, further subclassifications of the line items presented, classified in a manner appropriate to the entity’s operations.

78 The detail provided in subclassifications depends on the requirements of Ind ASs and on the size, nature and function of the amounts involved. An entity also uses the factors set out in paragraph 58 to decide the basis of subclassification. The disclosures vary for each item, for example:

(a) items of property, plant and equipment are disaggregated into classes in accordance with Ind AS 16;

(b) receivables are disaggregated into amounts receivable from trade customers, receivables from related parties, prepayments and other amounts;

(c) inventories are disaggregated, in accordance with Ind AS 2, Inventories, into classifications such as merchandise, production supplies, materials, work in progress and finished goods;

(d) provisions are disaggregated into provisions for employee benefits and other items; and

(e) equity capital and reserves are disaggregated into various classes, such as paid-in capital, share premium and reserves.

79 An entity shall disclose the following, either in the balance sheet or the statement of changes in equity, or in the notes:

(a) for each class of share capital:

(i) the number of shares authorised;

(ii) the number of shares issued and fully paid, and issued but not fully paid;

(iii) par value per share, or that the shares have no par value;

(iv) a reconciliation of the number of shares outstanding at the beginning and at the end of the period;

(v) the rights, preferences and restrictions attaching to that class including restrictions on the distribution of dividends and the repayment of capital;

(vi) shares in the entity held by the entity or by its subsidiaries or associates; and

(vii) shares reserved for issue under options and contracts for the sale of shares, including terms and amounts; and

(b) a description of the nature and purpose of each reserve within equity.

80 An entity whose capital is not limited by shares eg, a company limited by guarantee, shall disclose information equivalent to that required by paragraph 79(a), showing changes during the period in each category of equity interest, and the rights, preferences and restrictions attaching to each category of equity interest.

80A If an entity has reclassified

(a) a puttable financial instrument classified as an equity instrument, or

(b) an instrument that imposes on the entity an obligation to deliver to another party a pro rata share of the net assets of the entity only on liquidation and is classified as an equity instrument between financial liabilities and equity, it shall disclose the amount reclassified into and out of each category (financial liabilities or equity), and the timing and reason for that reclassification.

Statement of Profit and Loss

81 [Refer Appendix 1]

81A The statement of profit and loss shall present, in addition to the profit or loss and other comprehensive income sections:

(a) profit or loss;

(b) total other comprehensive income;

(c) comprehensive income for the period, being the total of profit or loss and other comprehensive income.

81B An entity shall present the following items, in addition to the profit or loss and other comprehensive income sections, as allocation of profit or loss and other comprehensive income for the period:

(a) profit or loss for the period attributable to:

(i) non-controlling interests, and

(ii) owners of the parent.

(b) comprehensive income for the period attributable to:

(i) non-controlling interests, and

(ii) owners of the parent.

Information to be presented in the profit or loss section of the statement of profit and loss

82 In addition to items required by other Ind ASs, the profit or loss section of the statement of profit and loss shall include line items that present the following amounts for the period:

revenue, presenting separately;

(i) interest revenue calculated using the effective interest method; and

(ii) insurance revenue (see Ind AS 117);

revenue, presenting separately interest revenue calculated using the effective interest method;

(aa) gains and losses arising from the derecognition of financial assets

measured at amortised cost;

insurance service expenses from contracts issued within the scope of Ind AS 117 (see Ind AS 117);

income or expenses from reinsurance contracts held (see Ind AS 117);

(b) finance costs;

(ba) impairment losses (including reversals of impairment losses or impairment gains) determined in accordance with Section 5.5 of Ind AS 109;

insurance finance income or expenses from contracts issued within the scope of Ind AS 117 (see Ind AS 117);

finance income or expenses from reinsurance contracts held (see Ind AS 117);

(c) share of the profit or loss of associates and joint ventures accounted for using the equity method;

(ca) if a financial asset is reclassified out of the amortised cost measurement category so that it is measured at fair value through profit or loss, any gain or loss arising from a difference between the previous amortised cost of the financial asset and its fair value at the reclassification date (as defined in Ind AS 109);

(cb) if a financial asset is reclassified out of the fair value through other comprehensive income measurement category so that it is measured at fair value through profit or loss, any cumulative gain or loss previously recognised in other comprehensive income that is

reclassified to profit or loss;

(d) tax expense;

(e) [Refer Appendix 1]

(ea) a single amount for the total of discontinued operations (see Ind AS 105).

(f)-(i) [Refer Appendix 1]

Information to be presented in the other comprehensive income section

82A The other comprehensive income section shall present line items for amounts of other comprehensive income in the period, classified by nature (including share of the other comprehensive income of associates and joint ventures accounted for using the equity method) and grouped into those that, in accordance with other Ind ASs:

(a) will not be reclassified subsequently to profit or loss; and

(b) will be reclassified subsequently to profit or loss when specific conditions are met.

The other comprehensive income section shall present line items for the amounts for the period of:

(a) items of other comprehensive income (excluding amounts in paragraph (b)), classified by nature and grouped into those that, in accordance with other Ind ASs:

(i) will not be reclassified subsequently to profit or loss; and

(ii) will be reclassified subsequently to profit or loss when specific conditions are met.

(b) the share of the other comprehensive income of associates and joint ventures accounted for using the equity method, separated into the share of items that, in accordance with other Ind ASs:

(i) will not be reclassified subsequently to profit or loss; and

(ii) will be reclassified subsequently to profit or loss when specific conditions are met.

83 [Refer Appendix 1]

84 [Refer Appendix 1]

85 An entity shall present additional line items, headings and subtotals in the statement of profit and loss, when such presentation is relevant to an understanding of the entity’s financial performance.

An entity shall present additional line items (including by disaggregating the line items listed in paragraph 82), headings and subtotals in the statement of profit and loss, when such presentation is relevant to an understanding of the entity’s financial performance.

When an entity presents subtotals in accordance with paragraph 85, those subtotals shall:

(a) be comprised of line items made up of amounts recognised and measured in accordance with Ind AS;

(b) be presented and labelled in a manner that makes the line items that constitute the subtotal clear and understandable;

(c) be consistent from period to period, in accordance with paragraph 45; and

(d) not be displayed with more prominence than the subtotals and totals required in Ind AS for the statement of profit and loss.

An entity shall present the line items in the statement of profit and loss that reconcile any subtotals presented in accordance with paragraph 85 with the subtotals or totals required in Ind AS for such statement.

86 Because the effects of an entity’s various activities, transactions and other events differ in frequency, potential for gain or loss and predictability, disclosing the components of financial performance assists users in understanding the financial performance achieved and in making projections of future financial performance. An entity includes additional line items in the statement of profit and loss, and it amends the descriptions used

and the ordering of items when this is necessary to explain the elements of financial performance. An entity considers factors including materiality and the nature and function of the items of income and expense. For example, a financial institution may amend the descriptions to provide information that is relevant to the operations of a financial institution. An entity does not offset income and expense items unless the criteria in

paragraph 32 are met.

87 An entity shall not present any items of income or expense as extraordinary items, in the statement of profit and loss or in the notes.

Profit or loss for the period

88 An entity shall recognise all items of income and expense in a period in profit or loss unless an Ind AS requires or permits otherwise.

89 Some Ind ASs specify circumstances when an entity recognises particular items outside profit or loss in the current period. Ind AS 8 specifies two such circumstances: the correction of errors and the effect of changes in accounting policies. Other Ind ASs require or permit components of other comprehensive income that meet the Framework’s definition of income or expense to be excluded from profit or loss (see paragraph 7).

Other comprehensive income for the period

90 An entity shall disclose the amount of income tax relating to each item of other comprehensive income, including reclassification adjustments, either in the statement of profit and loss or in the notes.

91 An entity may present items of other comprehensive income either:

(a) net of related tax effects, or

(b) before related tax effects with one amount shown for the aggregate amount of income tax relating to those items.

If an entity elects alternative (b), it shall allocate the tax between the items that might be reclassified subsequently to the profit or loss section and those that will not be reclassified subsequently to the profit or loss section.

92 An entity shall disclose reclassification adjustments relating to components of other comprehensive income.

93 Other Ind ASs specify whether and when amounts previously recognised in other comprehensive income are reclassified to profit or loss. Such reclassifications are referred to in this Standard as reclassification adjustments. A reclassification adjustment is included with the related component of other comprehensive income in the period that the adjustment is reclassified to profit or loss. These amounts may have been recognised in other comprehensive income as unrealised gains in the current or previous periods. Those unrealised gains must be deducted from other comprehensive income in the period in which the realised gains are reclassified to profit or loss to avoid including them in total comprehensive income twice.

94 An entity may present reclassification adjustments in the statement of profit and loss or in the notes. An entity presenting reclassification adjustments in the notes presents the items of other comprehensive income after any related reclassification adjustments.

95 Reclassification adjustments arise, for example, on disposal of a foreign operation (see Ind AS 21) and when some hedged forecast cash flow affect profit or loss (see paragraph 6.5.11(d) of Ind AS109 in relation to cash flow hedges).

96 Reclassification adjustments do not arise on changes in revaluation surplus recognised in accordance with Ind AS 16 or Ind AS 38 or on reameasurements of defined benefit plans recognised in accordance with Ind AS 19. These components are recognised in other comprehensive income and are not reclassified to profit or loss in subsequent periods. Changes in revaluation surplus may be transferred to retained earnings in subsequent

periods as the asset is used or when it is derecognised (see Ind AS 16 and Ind AS 38). In accordance with Ind AS 109, reclassification adjustments do not arise if a cash flow hedge or the accounting for the time value of an option (or the forward element of a forward contract or the foreign currency basis spread of a financial instrument) result in amounts that are removed from the cash flow hedge reserve or a separate component of equity, respectively, and included directly in the initial cost or other carrying amount of an asset or a liability. These amounts are directly transferred to assets or liabilities.

Information to be presented in the statement of profit and loss or in the notes

97 When items of income or expense are material, an entity shall disclose their nature and amount separately.

98 Circumstances that would give rise to the separate disclosure of items of income and expense include:

(a) write-downs of inventories to net realisable value or of property, plant and equipment to recoverable amount, as well as reversals of such write-downs;

(b) restructurings of the activities of an entity and reversals of any provisions for the costs of restructuring;

(c) disposals of items of property, plant and equipment;

(d) disposals of investments;

(e) discontinued operations;

(f) litigation settlements; and

(g) other reversals of provisions.

99 An entity shall present an analysis of expenses recognised in profit or loss using a classification based on the nature of expense method.

100 Entities are encouraged to present the analysis in paragraph 99 in the statement of profit and loss.

101 Expenses are subclassified to highlight components of financial performance that may differ in terms of frequency, potential for gain or loss and predictability. This analysis is provided in the form as described in paragraph 102.

102 In the analysis based on the ‘nature of expense’ method, an entity aggregates expenses within profit or loss according to their nature (for example, depreciation, purchases of materials, transport costs, employee benefits and advertising costs), and does not reallocate them among functions within the entity. This method is simple to apply because no allocations of expenses to functional classifications are necessary. An example of a classification using the nature of expense method is as follows:

Revenue X

Other income X

Changes in inventories of finished goods and work

in progress X

Raw materials and consumables used X

Employee benefits expense X

Depreciation and amortisation expense X

Other expenses X

Total expenses (X)

Profit before tax X

103 [Refer Appendix 1]

104 [Refer Appendix 1]

105 [Refer Appendix 1]

Statement of changes in equity

Information to be presented in the statement of changes in equity

106 An entity shall present a statement of changes in equity as required by paragraph 10. The statement of changes in equity includes the following information:

(a) total comprehensive income for the period, showing separately the total amounts attributable to owners of the parent and to non-controlling interests;

(b) for each component of equity, the effects of retrospective application or retrospective restatement recognised in accordance with Ind AS 8;

(c) [Refer Appendix 1]

(d) for each component of equity, a reconciliation between the carrying amount at the beginning and the end of the period, separately (as a minimum) disclosing changes resulting from:

(i) profit or loss;

(ii) other comprehensive income;

(iii) transactions with owners in their capacity as owners, showing separately contributions by and distributions to owners and changes in ownership interests in subsidiaries that do not result in a loss of control; and

(iv) any item recognised directly in equity such as amount recognised directly in equity as capital reserve with paragraph 36A of Ind AS 103.

Information to be presented in the statement of changes in equity or in the notes 106A For each component of equity an entity shall present, either in the statement of changes in equity or in the notes, an analysis of other comprehensive income by item (see paragraph 106 (d) (ii)).

107 An entity shall present, either in the statement of changes in equity or in the notes, the amount of dividends recognised as distributions to owners during the period, and the related amount of dividends per share.

108 In paragraph 106, the components of equity include, for example, each class of contributed equity, the accumulated balance of each class of other comprehensive income and retained earnings.

109 Changes in an entity’s equity between the beginning and the end of the reporting period reflect the increase or decrease in its net assets during the period. Except for changes resulting from transactions with owners in their capacity as owners (such as equity contributions, reacquisitions of the entity’s own equity instruments and dividends) and transaction costs directly related to such transactions, the overall change in equity during a period represents the total amount of income and expense, including gains and losses, generated by the entity’s activities during that period.

110 Ind AS 8 requires retrospective adjustments to effect changes in accounting policies, to the extent practicable, except when the transition provisions in another Ind AS require otherwise. Ind AS 8 also requires restatements to correct errors to be made retrospectively, to the extent practicable. Retrospective adjustments and retrospective restatements are not changes in equity but they are adjustments to the opening balance of retained earnings, except when an Ind AS requires retrospective adjustment of another component of equity. Paragraph 106(b) requires disclosure in the statement of changes in equity of the total adjustment to each component of equity resulting from changes in accounting policies and, separately, from corrections of errors. These adjustments are disclosed for each prior period and the beginning of the period.

Statement of cash flows

111 Cash flow information provides users of financial statements with a basis to assess the ability of the entity to generate cash and cash equivalents and the needs of the entity to utilise those cash flows. Ind AS 7 sets out requirements for the presentation and disclosure of cash flow information.

Notes

Structure

112 The notes shall:

(a) present information about the basis of preparation of the financial statements and the specific accounting policies used in accordance with paragraphs 117–124; (b) disclose the information required by Ind ASs that is not presented elsewhere in the financial statements; and

(c) provide information that is not presented elsewhere in the financial statements, but is relevant to an understanding of any of them.

113 An entity shall present notes in a systematic manner. An entity shall cross-reference each item in the balance sheet and in the statement of profit and loss, and in the statements of changes in equity and of cash flows to any related information in the notes.

An entity shall present notes in a systematic manner. In determining a systematic manner, the entity shall consider the effect on the understandability and comparability of its financial statements. An entity shall cross-reference each item in the balance sheet and in the statement of profit and loss, and in the statements of changes in equity and of cash flows to any related information in the notes.

114 An entity normally presents notes in the following order, to assist users to understand the financial statements and to compare them with financial statements of other entities:

(a) statement of compliance with Ind ASs (see paragraph 16);

(b) summary of significant accounting policies applied (see paragraph 117);